[ad_1]

SergeYatunin/iStock Editorial via Getty Photos

Introduction Thesis

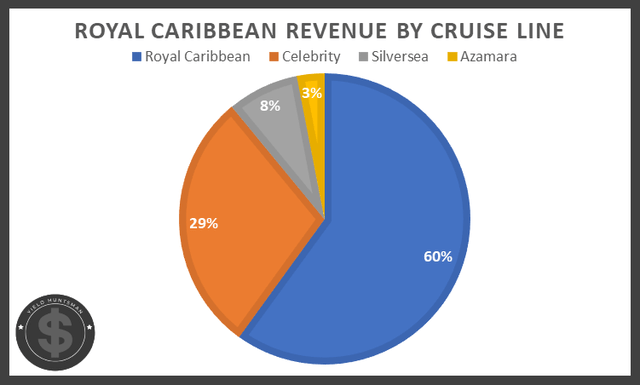

Royal Caribbean Cruises (NYSE:RCL) operates via 3 primary cruise traces to deliver a multitude of cruising itineraries about the globe. The corporation currently capabilities with 62 passenger ships, together with 5 of the world’s biggest, with an more 11 on buy for eventual provider. With 54 yrs of experience in the market, it has completed an exceptional task with capitalizing on the prospective its ships have and monetizing travellers to the finest of its means. Its blended 24% share of the international cruising marketplace areas RCL 2nd in passenger potential and allows diversification both of those in terms of price tag and out there itineraries.

Yield Huntsman and Royal Caribbean Cruises

These lines, at one particular issue, contributed to a lot more than $10B in yearly earnings nevertheless, extra a short while ago, they produced a mere fifth of what they the moment did. Reflecting this, share charges fell from all-time highs all around $135 to the lower $20s, and following a brief recovery, shares are again investing at an incredibly minimal valuation. With ship occupancy rates regularly trending higher, a quantity of operational enhancements must help in driving shareholder returns properly previously mentioned their historic highs. In blend with share price ranges achieving a sizeable degree of technical aid, now is an exceptional time to build a posture in Royal Caribbean Cruises.

Enhancing Operations

It is no question tough to search past the money issues introduced on by the Coronavirus, in particular in the cruising sector. However, Royal Caribbean boasts enhancements to a number of vital metrics that must, finally, outweigh the complications confronted in the course of considerably of 2020 and 2021. Empowered by an enhancing fleet of ships, higher occupancy fees are permitting the enterprise to get edge of the greatest revenue per passenger witnessed. Increase in its capability to adjust charges accordingly, Royal Caribbean really should exit the pandemic operationally stronger than at any time.

Further Ships

Because the commencing of 2021, 5 amazing ships have been additional to the, now, 100% operating fleet. Specified every marketplace in which it operates, except China, is now open for cruising, Royal Caribbean intends to just take full edge of its ship-creating qualities with the planned addition of 10 vessels. These more ships, which include a new “Icon Course” that’s expected to accomplish alongside its greatest ships in conditions of sizing, are intended to incorporate to the now-positive working cash move. The continued fleet growth alerts not only the supplemental desire that the business is facing from vacationers but the certainty amongst administration that these investments are worthwhile.

Higher Load Components

Even though not yet at pre-pandemic concentrations, strong ship occupancy premiums are predicted to carry on soaring, even with a more substantial fleet for travellers to fill. As of the to start with quarter, ships were being running with close to 68% of their rooms occupied this figure was anticipated to be in the higher 70% vary by the time they report Q2 earnings (August 2nd). In spite of reduce load elements, bookings for this interval are looking immensely potent in conditions of cruising demand. Main Govt Officer Jason Liberty experienced the adhering to to say during the first quarter earnings simply call:

Bookings improved each and every 7 days for the duration of the 1st quarter, as the effects from Omicron light. For the past 8 weeks, bookings have been meaningfully better than 2019 with particular strength in North American itineraries” (Q1 Earnings Get in touch with).

The good thing is, Royal Caribbean is not having for granted this possibility to closely monetize extra passengers when, in the latest decades, it really is been not able to. In transform, this has yielded history profits per passenger that should proceed when load elements return to regular.

Record Revenues Per Passenger

Creating use of each additional ships and larger sized crowds remaining brought to its cruise lines, Royal Caribbean has lately recorded its highest-at any time income for every passenger. Versus the identical interval in 2019, earnings for every visitor is up 4% and management attributes this feat largely to its recently implemented pre-cruise organizing technique that incentivizes better paying ahead of even location foot on its ships. These shopper deposit balances improved by $400 million throughout the very first quarter and point to better expending not only on latest voyages but also on long term cruises, considering 27% of these credits are finally devoted to these expenses.

Pricing Versatility

As cruise capacity increases, management is also getting note of its passengers’ willingness to spend while both equally scheduling and on their vacations. As you can visualize, ship occupants are fairly constrained in conditions of paying for food stuff and simple requirements, and with that, Royal Caribbean is performing to increase its rates appropriately. Specifically desirable is its observation that passengers easily accommodate these heightened costs offered the cruise ecosystem.

[W]hat we do see is as the client starts to gravitate to bigger pricing, as they get calibrated to what they are having to pay for a hotel room, or they are having to pay for other companies and dining establishments and so forth” (Q1 Earnings Phone).

With an maximize in travellers that can be accommodated, the potential to even further monetize explained customers really should translate into a long term of enormous revenue for Royal Caribbean.

Valuation

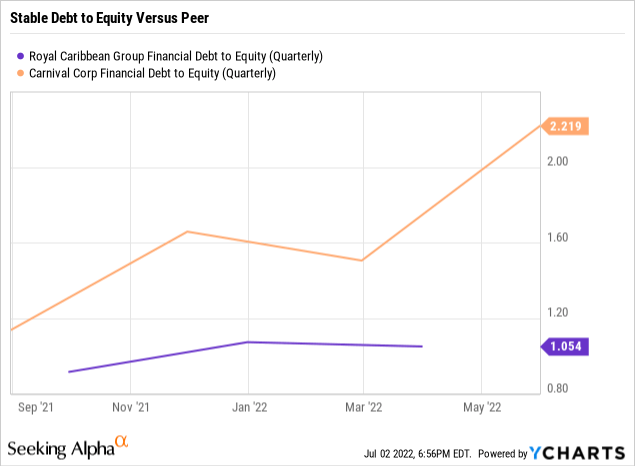

The decline of profitability for Royal Caribbean tends to make selected valuation strategies comparatively challenging, specifically when accounting for its formerly robust earnings. Irrespective of this, administration expects profitability for the latter 50 % of 2022 and mixed with lessening debt masses and enhancing functions, the existing valuation appears to offer you a deep discounted to what is achievable in the coming months as soon as the stability sheet has generally recovered. In looking to general public comparables to gain an knowing of where by Royal Caribbean stands, it appears to be competition like Carnival Corporation (CCL) are sustaining significant financial debt ranges irrespective of no near-time period anticipations of profitability. On the other hand, Royal Caribbean has been spending off better-fascination credit card debt thanks to its touted liquidity and refinancing remarkable loans.

Compared with friends, constrained leverage is staying set to use by Royal Caribbean (demonstrated by a moderate Credit card debt to Fairness Ratio) to equally maintain and expand functions. Its more compact personal debt loads are especially interesting in mixture with superior liquidity that must permit it to climate most extra, quick-time period, problems. As Chief Monetary Officer Naftali Holtz stated in the firm’s initially quarter earnings get in touch with:

Ending the quarter with $3.8 billion in liquidity. We have ample liquidity to enable us to continue our recovery trajectory” (Q1 Earnings Call).

This strong, and improving upon, equilibrium sheet should really relieve latest fears that have put huge tension on the firm’s valuation on top of that, measures are being place into location to counter foreseeable future dangers to its recovery.

Threats Relocating Forward

Inspite of the operational enhancements highlighted earlier mentioned, the hazards which initiated this steep slide in profits keep on being to some extent on the other hand, administration is entirely acknowledging these challenges and going to limit their affect. Outside of the clear impacts of the Coronavirus, heightened inflation and gasoline price ranges continue to present a average degree of hazard to Royal Caribbean’s return to normalcy. On the previous, inflation has prompted price ranges for most food items and staff members to maximize nonetheless, supplied the previously-pointed out pricing power that cruises retain given their enclosed environments, this possibility has been mitigated rather effectively as price ranges onboard can easily raise in line with inflation. Turning to gasoline selling prices, administration overtly reviewed this risk and manufactured point out of what it really is performing to reduce this issue:

On the fuel aspect, we keep on to improve use and have partly hedged rate beneath market place price ranges, which is mitigating the effect on our gas prices” (Q1 Earnings Phone).

In addition to hedging 55% of its gas fees for 2022, 8 of the company’s most recent ships are in the array of 30%-35% additional gas-successful than their predecessors. This craze is set to go on presented the prepared implementation of liquefied natural gas. This fuel is less expensive than minimal-sulfur fuel utilised by other ships and also less-putting on on motor elements, with each other, creating a much more value-economical alternative to continued sailing.

Specialized Examination

As shares trade at charges not seen because cruising was suspended around the globe, the opportunity for a strong comeback now is much more powerful than it was then. Elementary toughness ought to go on improving in light of the several favorable trends. Contemplating the risks which investors have priced in and the capability for management to change appropriately to these prospective difficulties, the selloff seems to supply an great prospect to establish a posture as income stream, and other metrics, change favourable.

TradingView

Primarily based off a channel that has formed about the previous two years, shares seem to be finding help earlier founded in the $30 location. This, coupled with an entrance into oversold territory according to the Relative Strength Index (RSI), factors to a promising short-term rebound in share selling prices. As this limited-term rebound happens, you can find a sturdy likelihood that the expected improvement in fundamentals carries on these gains, maybe to stages accomplished in 2021.

Final Ideas

Fearing whether Royal Caribbean had a practical strategy to overcome added worries in each the in the vicinity of and long expression long run, share prices now trade really near to the place they were being for the duration of the Covid-induced crash of 2020. Despite these fears, many catalysts have placed Royal Caribbean on an excellent trajectory for both equally its recovery and foreseeable future growth. In purchase to consider benefit of these promising traits, in particular as complex elements search to ignite a short-time period boost in share selling prices, now appears to be an excellent time to build a posture prior to this immense price becoming recognized.

[ad_2]

Resource connection